The 2026 Publishing Correction: Surviving the Post-Pandemic Market Reset

A definitive white paper analyzing the 2024-2026 market correction. We deconstruct the decline in print volume, the rise of AI-driven operations, and the impera

1. The Macro-Correction: Anatomy of a Downturn

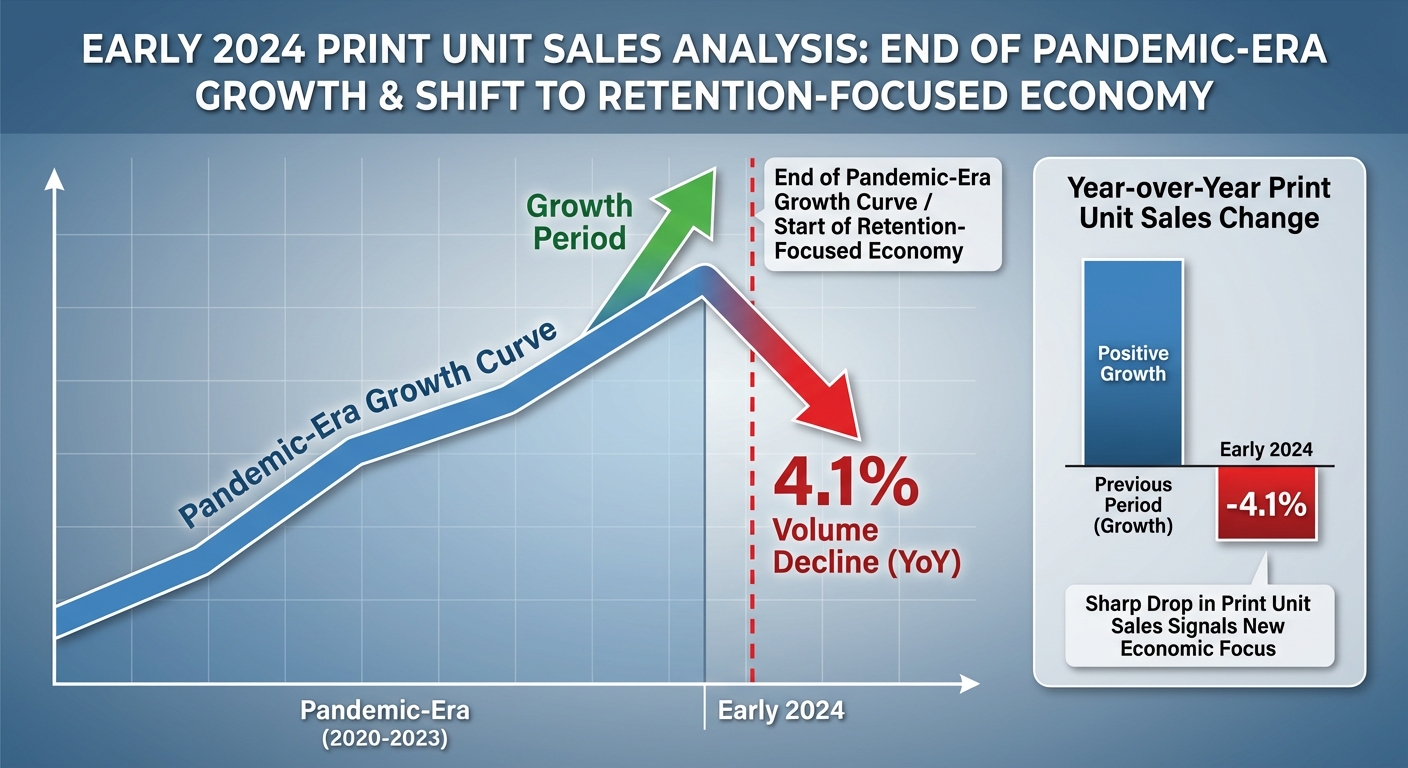

The data is unambiguous: publishing industry trends in 2026 point to a significant correction reshaping the market. Following the historic highs of 2020-2022, where captive audiences drove unprecedented engagement, consumer habits have reverted to the mean. This is not merely a 'cooling off'; it is a fundamental recalibration of demand. Reports from Publishers Weekly indicate that unit sales in key categories like adult non-fiction and juvenile fiction are trailing significantly behind previous benchmarks.

This contraction is exacerbated by inflationary pressures. As the cost of paper, shipping, and warehousing rises, publishers have raised cover prices, testing the price elasticity of the average reader. The result is a 'value gap' where casual readers are abandoning the format for cheaper entertainment alternatives (streaming, social media), leaving only the core super-readers.

The strategic implication is that 'volume' can no longer be the primary KPI. In a shrinking market, profitability must come from margin expansion (Direct-to-Consumer) and format diversification (Audio), rather than raw unit velocity.

Nuance: The Backlist Recession

For the past decade, backlist titles (books older than one year) have been the cash cow of the industry, often accounting for 60-70% of revenue. However, the current downturn is uniquely impacting this segment. Without the viral discovery mechanisms of a captive lockdown audience (e.g., BookTok's 2021 peak), older titles are fading into obscurity faster.

Publishers can no longer rely on passive backlist income to subsidize risky frontlist launches. Every title must now fight for active visibility, requiring a 'perpetual launch' marketing strategy rather than a 'set and forget' approach.

2. The AI Supply Chain: From Creation to Commerce

While the industry debates the ethics of AI writing, the operational revolution is already underway. Forbes analysis highlights that the true utility of AI in 2026 is not in replacing authors, but in replacing the 'mid-office' friction of publishing. This includes automated metadata optimization, dynamic pricing algorithms, and predictive inventory management.

We are witnessing the rise of 'Agentic Publishing.' AI agents can now monitor global trends, suggest cover design variations based on click-through data, and even re-write book descriptions in real-time to match trending search queries. This allows independent authors and agile publishers to operate with the sophistication of a multinational conglomerate at a fraction of the headcount.

Nuance: The Copyright Minefield

The edge case here is legal liability. As the courts debate the legality of training data, publishers utilizing AI-generated art or text risk having their copyright protections stripped. The US Copyright Office has been clear: purely AI-generated works are not copyrightable.

Therefore, the 'Human-in-the-Loop' is not just a quality control measure; it is a legal necessity. Authors must document the human creative input in every AI-assisted workflow to preserve the asset value of their Intellectual Property.

3. The Audio-First Pivot

While print contracts, digital audio expands. The modern consumer's lifestyle is increasingly incompatible with deep, focused reading but perfectly aligned with passive listening. The 'Audio-First' strategy is no longer a secondary consideration; for many non-fiction genres, it is the primary revenue driver.

The barrier to entry, namely the cost of production, has collapsed. AI narration (increasingly indistinguishable from human voice for non-fiction) allows for the rapid deployment of audio versions for backlist titles that previously did not justify the $5,000 studio investment. This unlocks a 'Long Tail' of audio revenue that was previously inaccessible.

"We are moving from a 'Reading Economy' to a 'Listening Economy.' If your book is not in ears, it does not exist for 30% of the market. - Forbes Tech Council"

Nuance: The Spotify Effect

The entry of Spotify into the audiobook market has fundamentally altered the royalty landscape. The 'streaming' model (paying per hour listened rather than per unit sold) favors long, engaging narratives over concise instructional content. Authors must now structure their books to maximize 'time on platform,' similar to how YouTubers optimize for watch time.

4. Direct-to-Consumer (DTC) Sovereignty

In a trending-down market, you cannot afford to rent your audience from Amazon. The most robust defense against the 2026 correction is the establishment of a Direct-to-Consumer (DTC) sales channel. This is the shift from 'Author' to 'eCommerce Brand.'

DTC allows for the capture of first-party data (emails, pixels) and the elimination of the 30-65% retailer tax. It enables the creation of bundles (e.g., Ebook + Audiobook + Video Course) that increase Average Order Value (AOV) significantly above the $9.99 ceiling imposed by Amazon's royalty tiers.

- Kickstarter Launches: Using crowdfunding not for funding, but for pre-validating demand and capturing high-value super-fans before the retail launch.

- Shopify Integration: Selling signed copies and merchandise directly to readers, turning a $20 book buyer into a $50 brand supporter.

- Sovereign Membership: Moving top readers off social media and into a paid Substack or Patreon community.

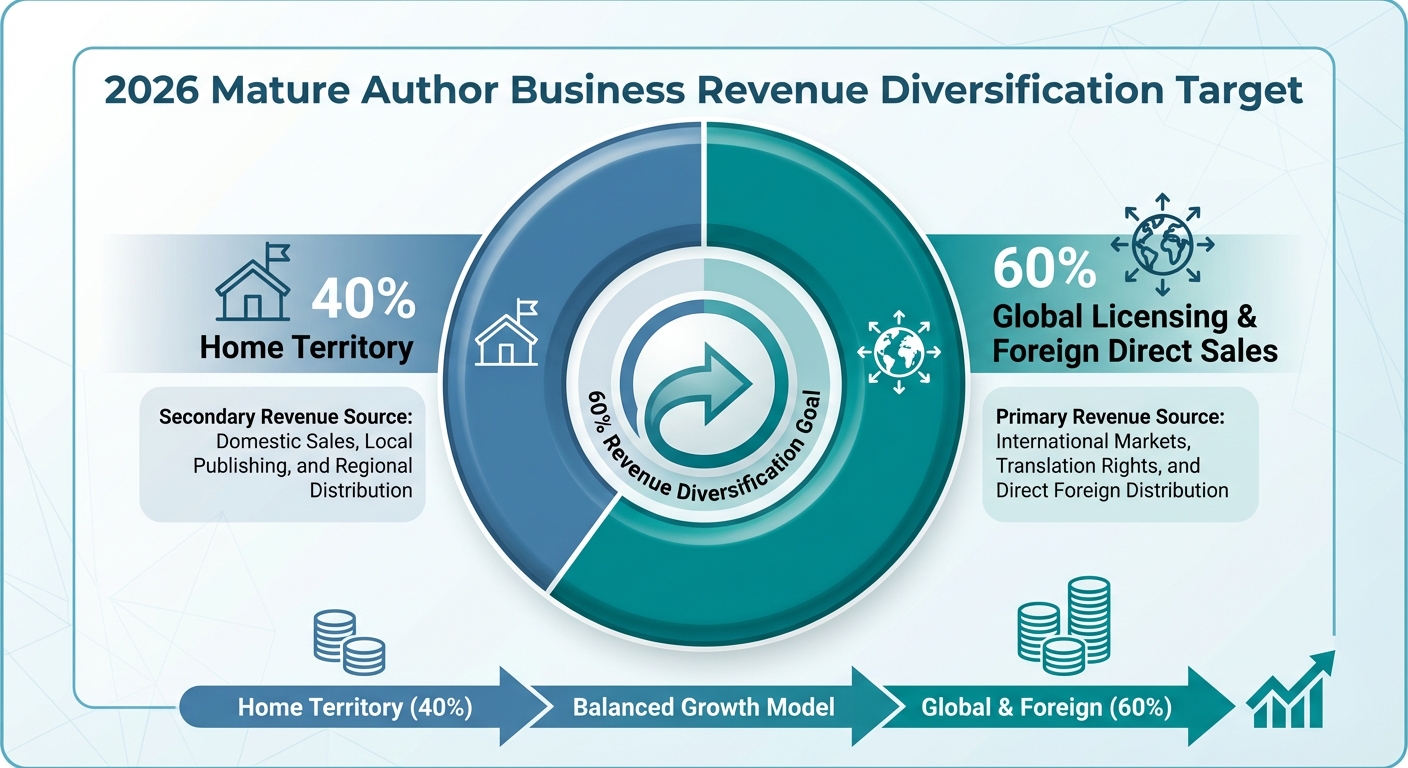

5. Global Rights Arbitrage

When the domestic market cools, the smart money moves offshore. Publishing Perspectives reports indicate that international rights trading is becoming a critical liquidity lever. Emerging markets in Asia and Latin America are not experiencing the same 'reading fatigue' as the West.

Independent authors are increasingly using 'Rights Arbitrage', retaining their English rights while aggressively licensing foreign language rights to territory-specific publishers. This diversifies the revenue stream; a slump in US sales can be offset by a surge in the German or Brazilian market.

Nuance: The Translation AI Bridge

Historically, translation was too expensive ($0.10-$0.15 per word) to justify for mid-list titles. The new protocol involves 'AI-First Translation' followed by 'Human Polish.' An AI translates the text to 95% accuracy, and a human native speaker edits for tone and idiom. This reduces costs by 70%, making it viable to launch simultaneous editions in Spanish, German, and French.

6. The Retail Renaissance: Experience Over Inventory

Finally, the role of the physical bookstore is evolving. As noted by Shelf Awareness, independent bookstores are surviving not by competing on inventory (Amazon wins there), but by competing on curation and community. For authors, this means the 'book tour' is dead, but the 'book event' is alive.

Retailers are favoring authors who can bring an 'experience' (a workshop, a tasting, a panel discussion) rather than just a reading. The physical space is for connection; the digital space is for transaction.

For independent author market data and annual earnings surveys, the Alliance of Independent Authors (ALLi) tracks how self-published authors navigate market corrections and platform shifts each year.